Introduction

You probably must have a heard a lot of buzz about a particular stock being over-valued or undervalued. These terms generally mean that the stock price is deviating from its intrinsic value, which is a range estimated for the stock price using fundamental modeling techniques like Discounted Cash Flow Model, Gordon Growth Model, etc.

A similar concrete valuation strategy is not yet established for cryptocurrencies, however there is a lot of literature and ideas floating around in academia which aim to achieve this feat.

In this post, I am going to go over a few of them.

So? Let’s get started!!!

Hot off academia! Measuring the P/E Ratio

You probably must have heard of the popular P/E ratio in finance, which measures the level of the current price of the stock with respect to its earnings (over the past 12 months). So, higher the PE ratio, the over-valued a particular stock is considered to be and vice versa.

Method 1:

In order to delineate something similar in the world of cryptos, we can consider the market price of the cryptocurrency to form the numerator, while the earnings can be proxied by “block rewards” and transaction fees paid by the users.

However, using transaction fees and block rewards as a proxy of fundamentals is misleading because these fees are earned by the miners and not by the token holders. Additionally there are a couple of other issues with this methodology. Generally a low P/E ratio is supposed to imply undervaluation of the asset. However, according to the above formula, a high spike in transaction fees could lower the PE ratio. This would in fact prevent users from transacting in the particular crypto, thereby bringing in undesirability into the asset (thereby making it overvalued).

Method 2

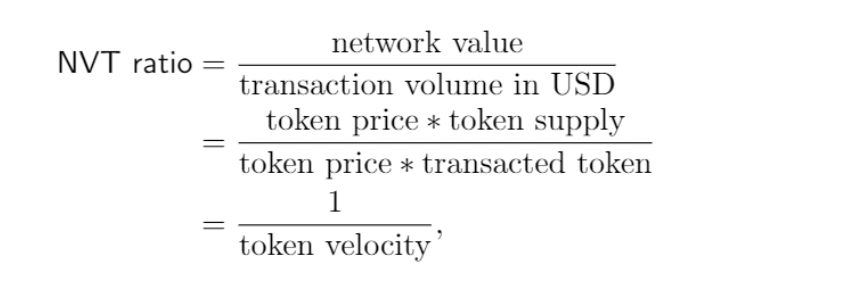

Another method used to create the PE ratio is based on network value. The Network-Value to Transactions ratio (NVT) utilizes the market cap of the crypto as the numerator and the crypto transaction volume in USD over the past 24 hours as the denominator.

We can intuitively interpret this ratio as a value which determines how frequently a crypto is used for transactions or how valuable a crypto is as a medium of exchange (for instance in the current world, the USD is treated as a reserve currency and a valuable medium of exchange).

A high NVT ratio indicates speculation and a low NVT ratio serves as a signal to buy the undervalued token.

That’s great but are there any drawbacks?

The limitation of the NVT ratio lies in the assumption that the fundamental value of a cryptocurrency is derived only from its function as a medium of exchange. But, there are a lot of inactive addresses out there, which just “buy-and-hold” crypto, so the usage of cryptocurrencies as a store of value is completely overlooked in this model.

Method 3

Metcalfe’s law

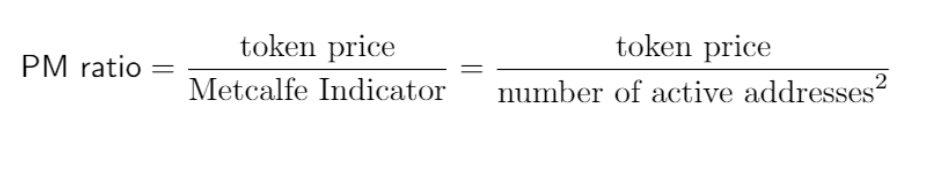

In the 1980s Robert Metcalfe, the inventor of Ethernet, proposed the value of a network is proportional to the square of the number of its users (see Shapiro and Varian (2010)).

The logic behind is that the number of connections of a network with n nodes is n(n-1)/2, which is asymptotically proportional to𝑛^2.

Since its inception, Metcalfe’s Law has become an influential tool for studying network effects. In crypto-economics, the number of Bitcoin active users is usually proxied by the number of active Bitcoin addresses. Therefore, the Price to Metcalfe’s (PM) Ratio can be formulated as follows:

Concluding Remarks

PM ratio exhibits a better potential as a valuation indicator for cryptocurrencies than P/E ratio and NVT ratio. However, it treats indifferently users with different amounts of tokens and overlooks the inactive users who hoard cryptocurrencies as a store of value.

All of them had their drawbacks, is there some super-duper alternative?

Well…of course of there is! But more on that in the next article.

Until then…

With Love,

From Coffee Time Finance,

Prarthana Shetty

One reply on “Valuation of Cryptocurrencies”

[…] More on that in the next article. […]

LikeLike