Setting the Context: Just like investors analyse different asset classes to allocate their investments, another style of investing is observing the exposure of the investment portfolio to different factors.

Factors are the drivers of return across different asset classes. For example, consider growth of GDP, it’s pretty intuitive that when an economy is performing well, the capital markets are in a better condition, so here GDP is called a macroeconomic factor. Next, consider the size of a company, you must have heard of “Large-Cap” and “Small-Cap” companies, this categorisation is usually done based on the market-capitalisation of a firm. Research suggests that in a stable economy, generally small-caps tend to outperform large-caps. So here, “Size” is another “factor”, it’s called a fundamental or a style factor.

So essentially we have two cohorts of factors, namely, macro-economic factors and style-based factors. To get a more detailed introduction to Factor Based Investing, check out Part I.

Research Run Through: Factor Investing in the light of COVID-19

By leveraging the power of Behavioural Finance and Factor Investing, portfolio managers can create portfolios which their clients would be comfortable sticking onto even during testing times.

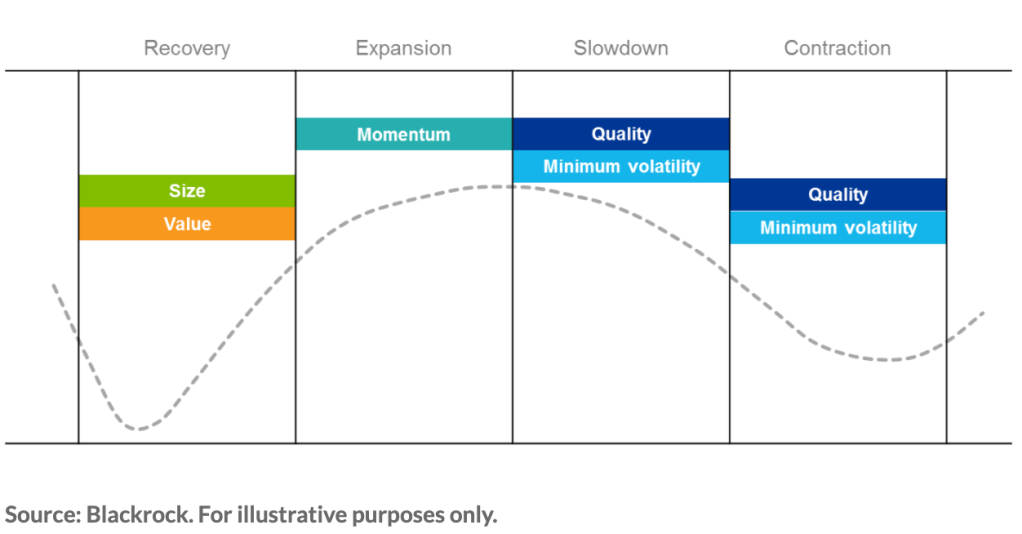

With the backdrop of the COVID-19 pandemic, let’s quickly go over how different single-factor based strategies perform given the circumstances (i.e. economic contraction).

The behaviour of factors could be quite predictable even in difficult times. In a bear market, using factors like Minimum Volatility have shown to be currently outpacing the SP500 index, while High Quality exposed portfolios have approximately been tracing along the index performance.

The Minimum Volatility Strategy focuses on lower risk and stable securities. This historically has delivered returns in line with the market. In a bear market scenario however, this strategy outpaces the rest because of it’s resilient nature (ability to tolerate higher levels of market volatility). However, do keep in mind, that this might not be the case IN ALL INSTANCES of market drawdowns.

To give you the quantitative figures, according to Black Rock research “minimum volatility has outperformed in 78% of rolling one-month drawdowns, but has outperformed in 100% of rolling six-month and one-year market drawdowns. With the time period in consideration being January 2011 – March 2020.” If you didn’t get that justification right now, it’s TOTALLY fine, I’ll go over how to perform quantitative analysis soon. 🙂

The Momentum Strategy, has a simple underlying principle, securities that have been performing well in the recent past, will continue performing well. In the current scenario (COVID-19 pandemic), minimum volatility stocks have been performing well, thereby the momentum based strategies would be picking up these high-performing securities. Therefore, we could say that there exists a high degree of correlation between the Minimum Volatility Strategy and Momentum Strategy, specifically in bear markets. However, please note, this correlation would change depending on the market cycle purely because of the cyclical behaviour of the factors. For example, in the recovery phase of the economic cycle, Value Based and Size Based factors tend to perform the best and these securities might be picked up by Momentum Based Strategies. To reiterate, Momentum based strategies focus on the trend of security performance and believe securities that have been performing well, will continue performing well.

The Quality Factor, focuses on picking securities which have stable earnings and clean balance sheets. Firms which have a safe haven of cash-reserves would strive better during turbulent winds. Thereby, using a “Quality Factor-Based Portfolio” would serve well during an economic slowdown. Simply because, these companies are better positioned than firms with unstable earnings or even high-growth startups, which might not have this safety net of cash reserves available to cushion them.

And that’s a wrap for this week! 🙂 Stay tuned for new articles every week, demystifying Finance for Gen A to Z.

Happy Learning,